SBP’s Guidelines on Loan Classification and Debt Relief

For someone struggling with loan payments, terms like “substandard” or “doubtful” can be confusing. However, understanding the State Bank of Pakistan’s (SBP) loan classification guidelines can be empowering. Moreover, these guidelines show how banks categorize loans by repayment status. They also influence how banks offer debt relief or engage in debt negotiation with borrowers.

In short, knowing these rules helps you grasp what happens when a loan goes bad and what options you have to fix the situation – including possible debt relief.

What Are SBP’s Loan Classification Guidelines?

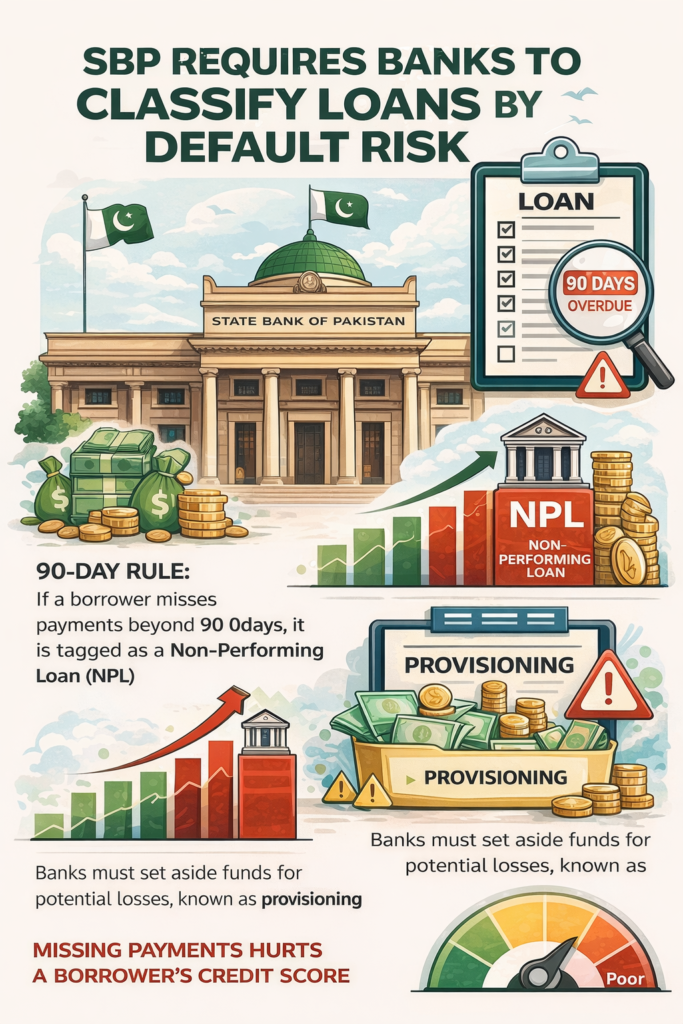

SBP, Pakistan’s central bank, requires banks to classify loans by the risk of default. If a borrower misses payments beyond a certain period (often 90 days), the bank must tag the loan as a non-performing loan (NPL). This system forces banks to recognize bad loans and set aside funds for potential losses (called provisioning). It also alerts borrowers that their credit standing is in jeopardy. In fact, many banking systems worldwide use a similar 90-day rule to identify default risk.

Under SBP’s guidelines, banks report NPLs to credit bureaus, so prolonged non-payment will hurt a borrower’s credit history. Thus, loan classification is a critical early warning mechanism. Understanding these categories is key to planning any debt relief or loan restructuring effort if you fall behind on a loan.

Categories of Classification

In general, banks in Pakistan label troubled loans in four main categories based on how late the payments are. Each category triggers a required provision (reserve) and signals the severity of the problem:

- Other Assets Especially Mentioned (OAEM) – Early warning category for loans up to 3 months overdue. Requires minimal provisioning (around 10% of the loan).

- Substandard – Loans over 90 days overdue (3–6 months of missed payments). The bank must provision about 25% of the loan amount as a potential loss. This status indicates serious delinquency.

- Doubtful – Loans over 180 days overdue (6+ months). The bank is required to provision around 50% of the loan amount. At this stage, the risk of default is very high.

- Loss – Loans over 12 months overdue. The bank must provision 100% of the loan (treating it as a loss). Essentially, the debt is viewed as defaulted, even if recovery efforts continue.

Consequently, moving through these categories has effects. For example, once a loan is substandard or worse, the bank stops counting it as income-generating and may step up recovery efforts. Moreover, the deeper a loan goes into doubtful or loss, the more likely the borrower will face legal action or a write-off. These classifications motivate both the bank and the borrower to address the issue early.

Debt Relief and Loan Restructuring

Loan classification is not just an accounting formality – it has real effects on banks and borrowers. When loans are classified as substandard or worse, banks must act. Additionally, they often prefer to help a borrower restructure the loan rather than wait for a complete default. For example, if you know you cannot catch up on payments, you should proactively contact your bank to discuss debt relief options (a form of debt negotiation, such as a temporary payment holiday). The bank might offer loan restructuring – adjusting the payment schedule, extending the term, or otherwise easing terms – to improve the chances of recovery.

SBP’s guidelines support loan rescheduling for borrowers in genuine financial difficulty. However, banks are cautioned not to use restructuring just to hide bad debts. Furthermore, any rescheduling should be backed by a viable repayment plan. Even after rescheduling a loan, it stays in the non-performing category until the borrower demonstrates good payment behavior for at least one year and repays a minimum portion (for instance, 10%) of the outstanding amount. Therefore, while restructuring gives relief, the borrower must follow through with the new plan to regain a “regular” status.

Early communication is critical. However, if a borrower waits until the loan is in the loss category, options narrow. At that late stage, banks may resort to legal remedies, and the chance for debt negotiation or concession is slim. By engaging the bank during the OAEM or substandard stage, you have a better shot at a solution. Notably, SBP has even provided temporary relief in crises: during COVID-19, it allowed banks to defer payments for one year without classifying those loans as defaults`. Such emergency steps are rare, so it’s prudent to seek an individual resolution long before situations escalate.

Loan Classification in Islamic Finance

In Islamic finance, banks follow the same loan classification rules as conventional banks. The contracts are Shariah-compliant (with profit instead of interest), but an overdue Islamic financing gets the same classification as an overdue conventional loan. Islamic banks also must make provisions for non-performing assets, similar to other banks. However, when Islamic finance customers default, the consequences under SBP guidelines are no different from any other loan – timely payment is vital to avoid classification and its fallout.

Loan Classification: Final Thoughts and Key Takeaways

Overall, SBP’s loan classification guidelines may seem technical, but they serve a simple purpose across conventional and Islamic finance: to flag troubled loans and prompt action. If you have a bank loan, pay attention to these warning categories. Falling into the OAEM or substandard range is a sign to take corrective steps – for example, by seeking debt negotiation or debt relief with your lender. By acting early, you can often work out a solution with your bank before the situation worsens.

In summary, understanding these guidelines helps you navigate debt problems more effectively. It equips you to engage with your bank from an informed position. Ultimately, the classification system protects both lenders and borrowers by encouraging transparency and early intervention. With knowledge of SBP’s rules, you can better manage your obligations and avoid the most severe consequences of loan default by seeking debt relief or a loan restructuring in time.