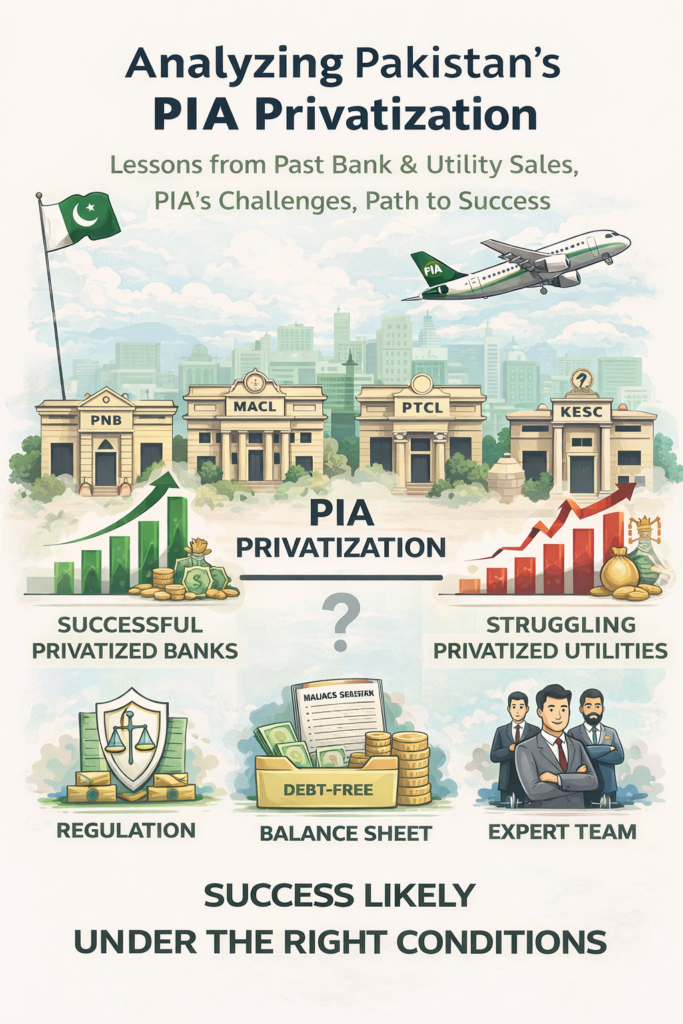

PIA PRIVATIZATION: HISTORY, PROSPECTS, AND LIKELY OUTCOME

Analyzing Pakistan’s PIA privatization: lessons from past bank and utility sales, PIA’s challenges, and why success is likely under the right conditions.

Privatization can mean many things, but at its core it’s transferring public assets to private hands to boost efficiency. Pakistan’s history shows mixed results. The privatizations of MCB, UBL, HBL and ABL (major banks) succeeded due to strong governance, central-bank oversight and clear profit motives. In contrast, utilities like PTCL (telecom) and Karachi Electric saw limited gains, often because of regulatory issues and lingering state interference.

The above examples set the stage for Pakistan International Airlines (PIA). Is PIA more like a bank or a utility in structure and fate? The evidence suggests PIA resembles the latter – a complex, politicized enterprise. However, after decades of losses (now over PKR 800 billion), new reforms have cleaned its balance sheet. With debt stripped out and Europe/UK flight bans lifted, PIA shows its first pretax profit in 20 years. If strategic buyers apply disciplined management and regulatory discipline is enforced, PIA can turn around. In my judgment, PIA privatization will likely succeed under defined conditions – namely full government exit and professional airline leadership – rather than fail outright.

Historical Lessons of Privatization: Banks vs. Utilities

Pakistan’s bank privatizations in the 1990s–2000s are seen as unqualified successes. In 1991 the state sold off MCB and Allied Bank, followed by HBL (2004) and UBL (2002). Afterward, about 80% of banking assets were in private hands. Studies show these banks saw far higher asset quality and profitability than state-owned peers. For example, earning-asset ratios jumped and nonperforming loans fell after privatization. The reasons were clear: new owners enforced strict governance and injected capital, while the State Bank strengthened regulations and oversight. Private banks also benefited from clear, market-driven business models in lending and deposits.

By contrast, utility privatizations have often stumbled. Pakistan Telecommunication Company (PTCL) was sold in 2005 (26% stake to Etisalat), but the process faced accusations of sweetheart deals and undervaluation. PTCL’s performance under private management lagged; profits slowed and service improvements were limited. Similarly, Karachi Electric (formerly KESC) was privatized in 2005 to address chronic outages. Yet, as one analyst noted, “two decades after handing Karachi Electric… to private investors, the city’s homes and businesses continue to suffer from repeat blackouts, erratic billing, [and] stalled investments”. In short, KE’s privatization did not end power shortages. These mixed outcomes reflect common issues: weak regulation and continued government interference in formerly public monopolies.

For clarity:

Privatization Successes (Banking Sector)

: MCB, ABL, UBL, HBL were revitalized under private ownership. New management enforced discipline; the SBP imposed strict supervision; and owners had clear profit targets.

Privatization Mixed Results (Utilities)

: PTCL and KESC saw limited service gains. Both remained monopolies with heavy regulation. Private investors often clashed with government policy, and investments lagged.

Overall, Pakistan’s privatization track record suggests: where strong regulation and clear commercial goals existed, outcomes were positive (banks); where political factors and monopoly power persisted, outcomes were disappointing (utilities).

PIA: More Like a Utility Than a Bank

PIA’s structure and problems align more with the “utilities” case. It is a large flag carrier, long burdened by politicization and monopoly rights on many routes. The government historically controlled its routes, pricing and leadership appointments. Like power companies, PIA had significant public obligations (e.g. unprofitable routes to remote areas) and suffered from overstaffing and political hires. In airlines, such interference creates inefficiency. For years PIA was flying with outdated planes and mismatched routes, unlike private global carriers that quickly cut losses on unprofitable flights. For example, under government ownership PIA was banned by European authorities (2018-2024) over concerns of pilot training, a self-inflicted blow to its most lucrative markets.

Privatized banks didn’t face such international compliance issues or aggressive competition, but airlines like PIA do. PIA competes globally and must meet strict safety and financial standards. These factors make PIA closer to a service monopoly under government sway than to a transparent profit-oriented business. In that sense, PIA is structurally nearer to PTCL/KESC scenarios than to the well-governed banks. On the other hand, a counterpoint: PIA does have professional staff and a recognizable brand, which could be harnessed in a free-market setting. But given its long history of losses and political meddling, the risk of failure loomed high unless the privatization framework is robust.

PIA’s Structural Realities

Any verdict on PIA must start with cold facts about its business. Decades of losses (roughly PKR 800+ billion debt) have crippled the airline. This chronic red ink came from a few sources:

Overstaffing & Political Hires

: PIA’s workforce ballooned due to political appointments. Budgets were strained by paying salaries to many unneeded employees.

Aging Fleet and Maintenance Issues

: Many PIA aircraft are old. Maintenance suffered from lack of funds, leading to grounding and cancellations. As one analysis noted, “a large number of the airline’s planes are very old… many aircraft are grounded and unable to fly,” weakening service and reputation.

International Restrictions

The EU ban (lifted in 2024) cut off major revenue. Restoring those routes through rehabilitation of safety standards improved the outlook.

Government Interference

Without autonomy, PIA often had uncommercial routes and priced tickets for political reasons.

Recent developments have addressed some of these realities. Under restructuring, Pakistan split off PIA’s debt into a Holding Company, leaving the Airline Company with clean operations. The government also assumed billions in legacy debt before the sale. Crucially, Western regulators have lifted bans on PIA flights after technical fixes. These moves mean the new owners can run the airline without an immediate pile of old liabilities dragging it down. Indeed, this year PIA posted its first pre-tax profit in twenty years, evidence that restructuring can work.

Who are the buyers now? The Arif Habib-led consortium (with Fatima Fertilizer, Fauji Fertilizer, etc.) paid PKR 135 billion (75% stake) and is buying the remaining 25% to take full control. These investors come from finance and industrial sectors, not airlines. On one hand, they have deep pockets (Rs125 billion committed for reforms). On the other, they lack aviation experience. This makes it imperative they hire or partner with airline professionals. If they do, their focus on returns could discipline PIA’s costs and service.

Core Question: PIA Closer to Banks or Utilities?

Summarizing, PIA behaves more like a former state-run utility or industrial SOE than a bank. Unlike banks, its product (air travel) is capital-intensive and globally competitive. Unlike privatized banks, it’s full of political baggage. The evidence in Pakistan suggests that enterprises with a banking model thrived after privatization, whereas heavy industries or utilities saw gains slip away. PIA’s decades of losses and political interference place it firmly in the latter camp.

However, there is one hopeful difference: airlines can be turned around quickly if run commercially. The holding-company debt-clearing (a form of financial engineering) is a tactical move rarely done for utilities. By isolating a “clean” airline entity, Pakistan is trying to give PIA the same fresh start banks got post-privatization. In that sense, PIA is a big, sick enterprise that needs aggressive rehabilitation, not incremental reform. The historical pattern warns caution, but targeted fixes could put PIA on a banking-like recovery path.

What Will Decide PIA’s Privatization Fate?

Whether PIA rises or falls under private ownership hinges on several factors:

Government Exit vs. Influence

A full handover is vital. The buyers insist on replacing government-appointed directors. If the new owners truly run PIA as their own company, away from political appointees, it can adopt commercial decision-making. (As one comment noted, complete sponsor change “will allow them to operate as a private entity, free from government-appointed board members”.) Conversely, any continued state meddling would likely undo progress.

Legacy Liabilities

The government has already cleared PIA of its legacy debt by moving it to the Holding Company. But will other obligations remain? For example, pension liabilities and unpaid supplier bills (the “circular debt” problem) must also be resolved. If PIA Airline still carries huge pension or debt payments, profitability will be weak. The ideal is that all unsustainable liabilities stay with the state, leaving the airline unencumbered.

Type of Buyer

Strategic vs. financial investors matter. The Arif Habib consortium is a mixed strategic group without direct airline pedigree. If they take a financial investor approach, focusing on costs and selling the company later, they might cut deep into workforce and assets to break even. If they seek a strategic partnership (e.g. with another airline or aircraft supplier), they could invest in fleet modernization and network integration. Global experience shows airlines often succeed post-privatization when a savvy carrier is involved (e.g. Tata-Vistara synergy for Air India). Thus, the buyer’s plan – to rebrand, raise capital and expand fleet as reported – will be a critical test.

Regulatory Environment

Civil Aviation Authority (CAA) must enforce safety and competition standards without shielding PIA unfairly. New owners will need freedom to set routes and fares competitively. At the same time, Pakistan’s regulators must ensure PIA meets IATA/IOS requirements (something that improved when bans were lifted). A clear, fair regulatory framework can prevent repetition of PTCL/KESC issues where contracts or tariffs were not enforced.

Workforce Restructuring

PIA likely needs much smaller, more skilled staff. Banks often succeeded by rightsizing, and PIA is no exception. The new owners plan “operational restructuring” which surely implies layoffs of redundant staff. This is politically sensitive, but necessary for efficiency. If handled with buyouts and retraining, it can reduce costs. Conversely, failure to cut headcount or enforce productivity will keep losses recurring.

In summary, conditions for success are concrete: government steps back fully, the buyer is serious (and possibly strategic), old debts/pensions stay with the state, and PIA is allowed to operate competitively. Absent these, the outcome would mirror Pakistan’s troubled utility sales, with only partial gains.

Global Comparisons: Airlines Privatization

Looking abroad offers a reality check. British Airways (BA) was privatized in 1987 and is often cited as a turnaround story. Under tough new management, BA went from losses to becoming “the world’s favorite airline” within a few years. That case shows that strong leadership and capital can revive a national carrier. However, BA’s success also came with strict cost-cutting and later joining a larger airline group, which may or may not directly apply to PIA.

Air India’s recent privatization is instructive too. Sold to Tata Group in 2021, Air India had been a money-loser under state ownership. The new private owner immediately began a massive overhaul (fleet renewal, route rationalization, brand relaunch) as reported by its CEO. The Indian government also bailed out most of Air India’s debt before sale, similar to Pakistan’s approach. Early signs suggest Air India’s turnaround is possible, given India’s huge market and the strategic buyer’s industry know-how. The common thread: when governments address debt and let capable private airlines or financiers take charge, flag carriers can bounce back.

By contrast, countries that privatized airlines without these conditions often struggled. For example, EgyptAir and India’s Jet Airways faced trouble despite private ownership because of market missteps or weak regulation. The lesson is that privatization alone isn’t magic; the buyers’ expertise and post-sale support matter. Since PIA’s transition is still fresh, Pakistan has a timely opportunity to apply these lessons effectively.

Will PIA Privatization Succeed?

After weighing the evidence, we conclude that PIA’s privatization is likely to succeed – but only under clearly defined conditions. This is not a vague “it depends,” but a focused forecast. On balance, Pakistan’s track record shows that when an enterprise is properly restructured, freed from political meddling, and handed to owners with skin in the game, efficiency improves. The cleaning of PIA’s balance sheet, the competitive bidding process, and the consortium’s sizable investment plan all point toward a real chance for turnaround.

Key Conditions for Successful PIA Privatization

However, this success requires the following: the government must exit fully (no more government-appointed boards), PIA’s old debts and pension liabilities must remain off the airline’s books, and the new owners must run PIA with commercial rigor rather than seeking subsidies. The consortium should ideally partner with experienced airline managers or international partners. If these conditions are met, PIA can harness private capital and discipline to modernize its fleet, optimize routes, and restore customer trust.

PIA Privatization: Success Likely Under Clear Conditions

In short, we predict PIA’s privatization will succeed under defined conditions. This verdict aligns with historical evidence: Pakistan’s privatized banks succeeded by shedding politics and focusing on business, whereas utilities failed when politics stayed involved. PIA, as a special case, can achieve the bank-style success if privatization is followed through completely. The risk of failure is real but avoidable – provided regulators stay strict, liabilities stay with the state, and private management is empowered to run PIA like any global airline. With those guardrails in place, Pakistan’s flagship carrier has a strong chance to emerge from privatization as a leaner, customer-focused airline, rather than a continued burden on the public.

Amer Malik

Founder & CEO – Desiche Konseltants

Amer Malik, former CEO of Islamic Modaraba Company, is a seasoned banker with 33 years of experience. He now leads Desiche Konseltants, offering financial mediation. His expertise spans Loan Restructuring, Debt Dispute Mediation & Resolution, Loan processing for Individual, SMEs, and strategic advisory.