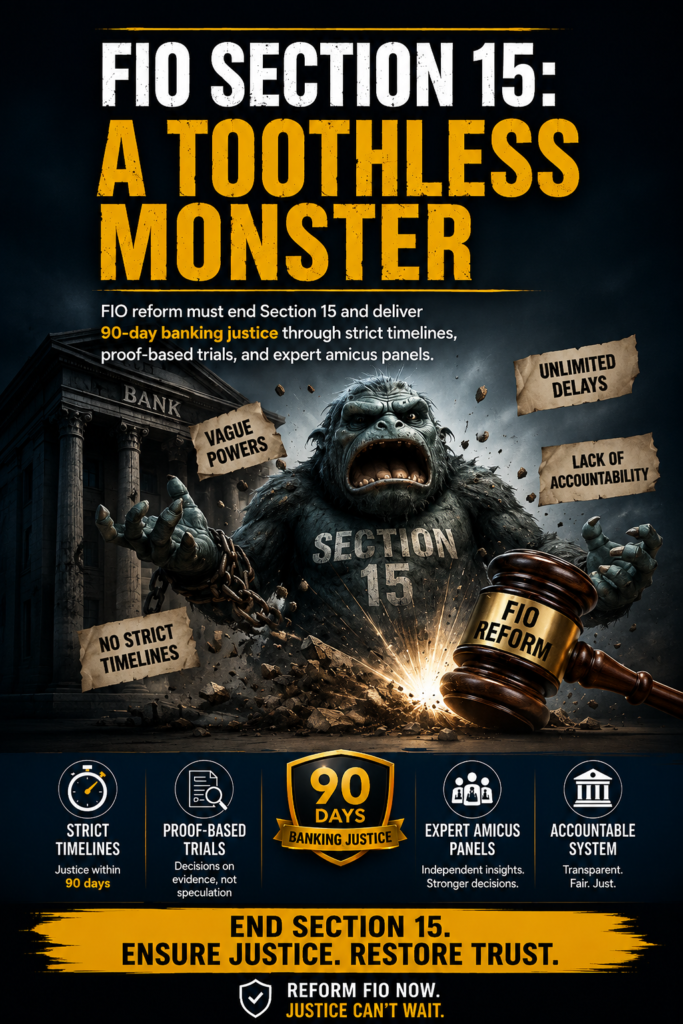

FIO reform must end Section 15 and deliver 90-day banking justice through strict timelines, proof-based trials, and expert amicus panels.

The case against Section 15

Pakistan’s Banking recovery law has remained irresolute for decades. Repeated special legislation especially Section 15 of FIO has failed to solve delays in banking recovery matters. At the same time, original jurisdiction in larger banking cases has continued to burden the superior Courts. The deeper problem lies elsewhere. A recovery system cannot succeed when its structure conflicts with the judicial system instead of strengthening and disciplining it.

Under the current compiled FIO text, claims above fifty million rupees still go to the High Court in original jurisdiction, even though the law also allows the Federal Government to create as many Banking Courts as needed. That split weakens specialization from the start.

One caution is necessary. As of this review, the Pakistan Code page still reflects the earlier consolidated FIO text, while parliamentary records show a 2026 amendment bill moving through the National Assembly and Senate lists. I therefore treat the 2026 changes as the latest passed bill text reflected in parliamentary materials, not yet as a fully consolidated code version on the Pakistan Code website.

Section 15 was sold as speed. Its core promise was stark. A bank could sell mortgaged property “without the intervention of any Court.” Yet, the same statutory scheme still sends the dispute back to the Courts once possession is resisted. It still requires the Banking Court to resolve disputes regarding the sale. Moreover, it still invites litigation over injunctions, notices, valuation, possession, and title. Therefore, the promise of speedy non-judicial recovery remains largely unfulfilled. A remedy bypassing Courts initially still returns to Courts during enforcement disputes.

The Unstable Legal Foundation of Section 15

That structural weakness explains why Section 15 has never become normal legal ground. In the constitutional history recounted by the Sindh High Court, the Lahore High Court first set the original Section 15 aside, and the Supreme Court upheld that result in National Bank of Pakistan and 117 others v. SAF Textile Limited and another PLD 2014 SC 283. The Courts focused on a simple defect. The old section extinguished property rights before borrowers could meaningfully challenge unfair or sham sales. That defect was not incidental. It was central to the mechanism itself.

The legislative response itself proves the weakness. Parliament rewrote Section 15 in 2016. Later, the 2018 Rules added more safeguards. These included Chartered Accountant reviews, Professional Valuers, and bidding procedures. Then, the Lahore High Court upheld the amended section in 2020. Now, the 2026 bill again seeks stronger enforcement powers through Deputy Commissioners and immunity clauses. Every amendment reflects the same reality. Section 15 still lacks stable legal footing. It survives only through repeated procedural protections.

Section 15: A Monster Without Teeth

That is why “toothless monster” is not a slogan. It is a diagnosis. Section 15 looks fierce on paper. However, every sharper version creates another front for challenge. The 2026 bill even contemplates administrative help to take possession and protect those acts from challenge. That may look efficient. Yet, in a rights-based system, a stronger ouster clause often pushes litigants toward constitutional review, not toward silence. The monster keeps growing new fangs. Still, it cannot bite through due process.

The real target is ninety days

The better answer is not to ask how to save Section 15. The better answer is to ask what FIO should truly deliver. The right target is final resolution within ninety days. It is not something completely new or outside the law. FIO already uses a proof-heavy model. A Plaint must carry a certified Statement of Account and relevant documents. A defendant must defend within thirty days with disputed facts, amounts, and supporting documents. A non-compliant leave application may be rejected. In short, the law already leans toward an evidence-first, delay-light design.

FIO also already contains the timing logic that reformers keep asking for. Once leave is granted, the suit is to be disposed of within ninety days. Adjournments should not exceed seven days except in extraordinary cases. Moreover, where evidence is needed, the law already permits affidavits for examination-in-chief. That is a modern procedural tool. New system will reduce wasted hearings. It supports a document-led process.

The Real Failure of FIO

So, the true failure is not lack of ideas. The true failure is weak enforcement of the ideas that FIO already contains. The legal system did not need a private foreclosure myth. It needed disciplined case management, more specialized judges, tighter control over side applications, and faster fact resolution inside Court.

Therefore, the policy goal should change. The question should no longer be: how do we help banks sell outside Court? The real question should be: how do we make Banking Courts finish recovery cases, fairly and firmly, within ninety days? That shift is both more honest and more constitutional. It accepts that coercive transfer of property sits near the core of judicial power. It also accepts that Pakistan’s legal culture will challenge any shortcut that looks like a parallel Court in private hands.

A better FIO in five reforms

First, repeal Section 15 as a private sale route.

FIO should stop pretending that non-judicial foreclosure can do the heavy lifting. The section still depends on Court-backed possession when resistance begins, and the Supreme Court’s critique of the old model struck at the absence of meaningful remedies before rights were extinguished. If Parliament now creates a renamed clone, including a housing-finance version under a new provision, it will only repackage the same defect. The system should admit failure and move on.

Second, place every original recovery suit before specialized Banking Courts.

Current FIO text still sends cases above fifty million rupees to the High Court in original jurisdiction. That split weakens speed and consistency. It should end. The High Court should hear appeals and constitutional cases, not run first-instance debt suits as a routine docket. Parliament does not need a new theory for this. FIO already lets the Federal Government establish as many Banking Courts as necessary. The law should now require that expansion.

Third, convert FIO into a hard calendar statute.

The law should say that cases below fifty million rupees must finish within ten hearings. Cases above fifty million should finish within fifteen hearings. Those caps should include all interlocutory matters. They should also work with what FIO already allows: affidavit evidence, document-heavy pleading, and a ninety-day disposal rule. Therefore, the amendment should turn today’s soft timeline into a mandatory timetable with automatic consequences for breach.

Fourth, stop frivolous collateral applications by express text.

Here, the answer is legislative discipline. FIO already overrides inconsistent laws and borrows the Civil Procedure Code only where FIO is silent. That means Parliament can expressly fence off delay tactics, including repetitive applications framed under inherent powers. A banking judge should hear only one such application from each side, unless wholly new facts arise. Every rejected frivolous application should trigger real costs and, where delay continues, a security deposit before the party may press further objections.

Fifth, and most importantly, build an Amicus Curiae Panel into the center of FIO.

This is the truly promising reform. Remarkably, FIO already contains the seed. Section 5(8) already allows a Banking Court to seek help from an amicus curia on technical banking issues, and it requires substantial banking experience and suitable qualifications. In addition, the Sindh High Court recently appointed an amicus in a Section 15 dispute involving valuation rules. That matters. It proves that Courts already turn to neutral expertise when the dispute becomes technical.

Desiche Konseltants would support a three-member amicus panel, which may fairly be called an Amicus Jury in substance, even if the statute should use the cleaner term “panel.” Each member should owe a duty to the Court, not to the parties. That duty is familiar in other civil systems. In England and Wales, Court experts and assessors assist the Court through specialized skill and expertise.

That model does not hand power to one litigant. Instead, it adds neutral technical judgment inside the judicial process.

The Amicus Panel Model for 90-Day Justice

The panel should work like this. Both sides must file all proofs at the start. The bank files finance documents, statements, notices, valuation material, and proof of default. The defendant files the leave application, disputed amount, and all supporting documents at once. The Banking Court then sends the live accounting, valuation, and document-authenticity issues to the amicus panel within seven days.

The panel holds one short hearing in smaller cases, and no more than two in larger ones. It then issues a reasoned majority report within thirty days. That majority report should bind the factual dispute, unless the judge finds fraud, clear bias, or patent illegality on the face of the record. The Court should then issue decree within ten days. In practical terms, the case ends when the majority decides. However, the final decree still comes from the Court, making the system legally stronger and harder to challenge.

That reform is revolutionary in the right way. It does not create a private foreclosure empire. It does not ask the Bank to become Judge, Auctioneer, and Dispossessor. Instead, it keeps the dispute inside the judicial system but strips out its worst delays. It also fits the reality of banking litigation. Many of these cases turn less on broad oral testimony and more on ledger analysis, markup calculations, notices, title papers, and valuation disputes. Neutral specialists can resolve those issues faster than endless adversarial skirmishing.

Amendments the statute now needs

The statutory roadmap is clear. First, amend section 2(b) so that all original recovery suits go to Banking Courts, regardless of value. Leave section 22 appeal jurisdiction intact.

Second, amend Section 5(1) to ensure sufficient Banking Courts based on region and case volume, instead of leaving Court expansion solely to administrative discretion.

Third, replace the current single-amicus language in sections 5(8) and 5(9) with a formal three-member Amicus Panel, backed by rules on disclosure, conflict checks, remuneration, timetable, and majority report.

Next, repeal Section 15 as a self-sale mechanism and repeal or revise related subordinate rules based on private foreclosure. If Parliament still seeks faster mortgage recovery, it should allow sale only after judicial determination, not before it. Otherwise, the same constitutional defect will merely shift from one section to another.

Procedural Discipline and the 90-Day Recovery Framework

Then tighten sections 9, 10, and 13. Section 9 should require a complete documentary record at filing. Under Section 10, no defense should survive without full documents and a precise disputed figure. Moreover, Section 13 should impose a ninety-day outer limit from completion of service, subject only to narrow exceptions for evasion or force majeure. It should also limit hearings to ten or fifteen, restrict adjournments, and require judgment within ten days. The section should limit hearings to ten or fifteen, restrict adjournments, and require judgment within ten days.

Finally, insert a new provision to kill frivolous interlocutory practice. That new section should state that any collateral application, including one invoking inherent powers, must be decided on the same date or within three working days on the papers. It should also state that a rejected frivolous application carries mandatory compensatory costs and, after a second failure, a security requirement.

Conclusion

The verdict is simple. Section 15 has consumed twenty-five years of reform energy and still has not delivered its founding promise. The Courts struck the old version for lack of safeguards. Parliament rebuilt it. The rules thickened it. The Courts upheld the rebuilt version. Parliament now wants to reinforce possession through district administration. Yet the same basic weakness remains. Section 15 is a parallel coercive track in a system that will keep dragging coercion back toward judicial scrutiny. That is why it feels powerful but performs weakly. It is, in truth, a toothless monster.

FIO should now abandon the illusion of private foreclosure and embrace the answer already hidden within the statute itself. The real solution is a Court-centered recovery model completed within ninety days. It should rely mainly on documents and remain protected from frivolous side litigation. It should also be strengthened through binding majority findings from neutral amicus experts. Pakistan does not need another attempt to sharpen Section 15. It needs the courage to bury a failed experiment and overhaul FIO. Speedy justice must return to where it constitutionally belongs: inside a disciplined and specialized Banking Court.