Myths About Bank Defaulter: Are You Being Judged Unfairly?

Introduction: When Circumstances Turn Against You

Yet the moment a loan goes unpaid, the reaction is swift. Labels appear. Judgments follow. The term “bank defaulter” suddenly carries weight far beyond the situation itself. It begins to suggest dishonesty, carelessness, even moral failure.

But pause for a moment; does every default really tell that story?

Many people who default never planned to. They took risks in good faith. They tried to grow and build businesses. Then something changed; something they could not fully control.

This is where the conversation needs correction. Because what we assume about defaulters often says more about our belief than their reality.

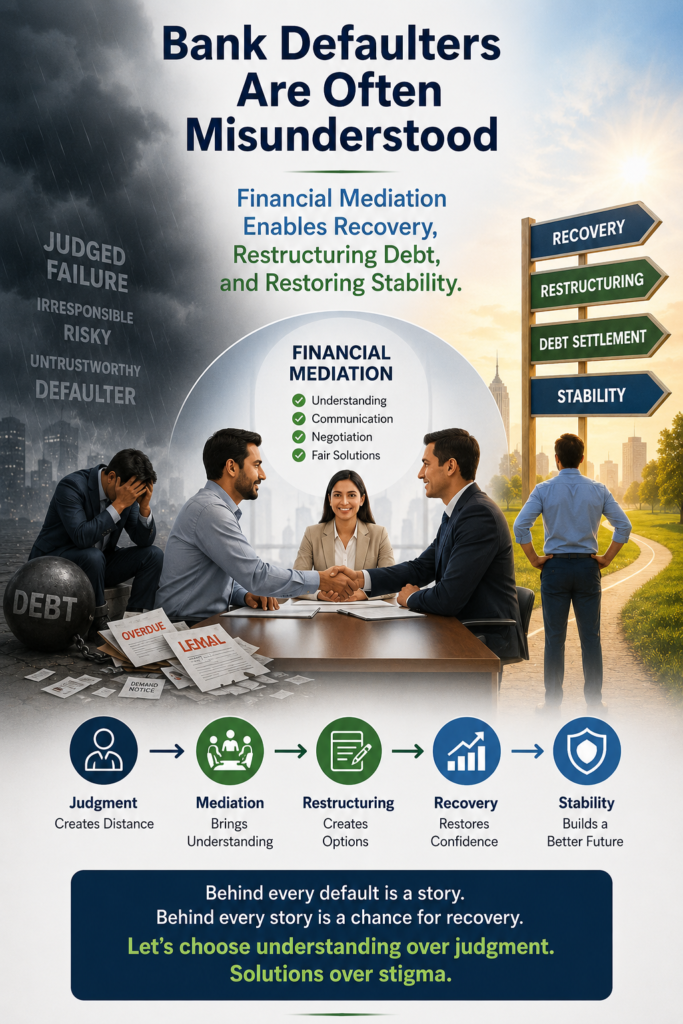

This article looks closely at those assumptions. It separates myth from truth. And more importantly, it shows how financial mediation can quietly rebuild what seems broken.

Time to Change the Narrative about Bank Defaulters

We tend to judge outcomes; not journeys. That is the first mistake.

A default is usually the end of a story we did not see. We do not see the months of effort, the decisions made under pressure, or the circumstances that changed everything.

Markets shift. Costs rose unexpectedly. Clients disappear. Health issues intervene.

So, when repayment stops, it doesn’t automatically mean someone failed morally. More often, it means the environment changed faster than the plan could adapt.

And yet, recovery is possible; very much so.

With the right structure, guidance, and communication, people do come back. Businesses are stabilizing. Debts get resolved. Confidence returns.

The real shift we need is simple:

move from blame to understanding; and from judgment to resolution.

Myth 1: “Being Bank Defaulter is a Willful Cheat”

This is perhaps the most common; and most damaging; belief.

It assumes intent without evidence. It paints everyone with the same brush. But reality is far more layered.

Many defaulters are simply people caught in situations they didn’t expect. A small trader loses supply due to import delays. A manufacturer struggles when currency swings and wipes out margins. A business owner faces a sudden drop in demand.

None of these scenarios begin with dishonesty. They begin with risk; and risk is part of growth.

In fact, many borrowers default not because they wanted to escape responsibility; but because they could no longer manage the burden created by changing conditions.

So before labeling someone, it’s worth asking:

What actually happened behind the scenes?

Myth 2: “Once You are a Bank Defaulter Default, Your Financial Life Is Over”

This belief is not only incorrect, it’s dangerous. It pushes people into hopelessness. It makes them think recovery is impossible. But financial systems, when used properly, are not designed to end journeys; they are designed to restructure them.

Loans can be renegotiated. Terms can be adjusted. Penalties can be reduced.

And with proper mediation, these adjustments don’t just happen randomly, they happen strategically.

Many borrowers who once defaulted have rebuilt stable positions. Some have even grown stronger than before.

The difference is not luck. It is guidance, structure, and prompt intervention.

Myth 3: “Bank Defaulter Avoid Communication”

On the surface, this seems true. Banks often complain that borrowers disappear. Calls go unanswered. Meetings get delayed.

But look deeper, and the picture changes.

Most people don’t avoid communication because they want to. They avoid it because they feel trapped.

There is fear of embarrassment, fear of pressure, fear of legal consequences.

So instead of facing the situation, they withdraw. And unfortunately, that silence makes everything worse.

This is where financial mediation changes the dynamic completely.

When a neutral, professional voice enters the conversation, tension reduces. Discussions become structured. Emotions step aside.

And suddenly, what felt impossible becomes manageable.

Myth 4: “You Can’t Recover After Default”

If that were true, many global success stories wouldn’t exist.

Failure, in many cases, comes before success; not after it.

A business that defaults today may simply be one that miscalculated timing, not capability. With the right adjustments, it can recover.

In fact, restructuring often forces discipline. It brings clarity. It removes inefficiencies.

And when credibility is rebuilt step by step, markets respond. Opportunities return.

Default, then, is not an ending. It is a difficult transition point.

Myth 5: “Islamic Finance Does Not Allow Restructuring of Bank Defaulter”

This misunderstanding comes from a superficial reading of principles. Islamic finance is not rigid; it is deeply rooted in fairness and compassion. The idea that a struggling debtor must be pressured without relief contradicts its spirit. In fact, the guidance encourages giving time, easing burden, and even showing generosity in hardship.

Modern Islamic financial frameworks also provide room for restructuring. Contracts can be adjusted within ethical boundaries. Solutions can be negotiated without violating core principles.

So rather than restricting options, Islamic finance actually supports humane solutions; when applied correctly.

Why Financial Mediation Matters

Traditional recovery methods often focus on pressure. Legal notices. Escalation. Litigation.

These methods may recover money; but often at a high cost. Relationships break. Stress increases. Time is lost.

Financial mediation takes a different path.

It focuses on understanding first, structure second, and resolution third.

Instead of forcing outcomes, it builds them; carefully and realistically.

It aligns expectations between borrower and bank. It introduces clarity where confusion existed. And importantly, it preserves dignity throughout the process.

That balance is what makes it effective.

The Human Side of Default

Behind every default is a person.

A person dealing with pressure, uncertainty, and often silent anxiety.

Yet society rarely sees that side. It sees numbers, labels, and outcomes; but not the emotional weight behind them. This lack of empathy creates distance. It discourages people from seeking help. And that delay makes recovery harder. If we want better financial outcomes, we need better understanding. Not softness; but fairness. Not judgment; but clarity.

How Desiche Konseltants Can Help

This is exactly where structured mediation becomes valuable.

Desiche Konseltants approaches financial distress with both discipline and understanding. It doesn’t just look at numbers; it looks at context.

The focus is still clear; resolve debt in a way that works; for both sides.

That includes preparing documentation, presenting structured proposals, negotiating realistic terms, and guiding borrowers through each step. Confidentiality stays intact. Judgment stays out of the room. And the process becomes something manageable; rather than overwhelming.

Conclusion

Not every bank defaulter is what society assumes.

Often, they are individuals who take risks, face setbacks, and find themselves in situations they did not fully control. The real issue is not default itself. It is how we respond to it.

If we continue to judge, we delay solutions.

If we choose to understand, we create them.

Financial mediation offers that path; balanced, practical, and human.

And perhaps that is the real shift we need:

not in systems, but in perspective.

Author Bio

Amer Malik

Founder & CEO – Desiche Konseltants

Amer Malik has over three decades of banking experience. He now leads Desiche Konseltants, focusing on structured financial mediation, ethical restructuring, and practical debt resolution across Pakistan.