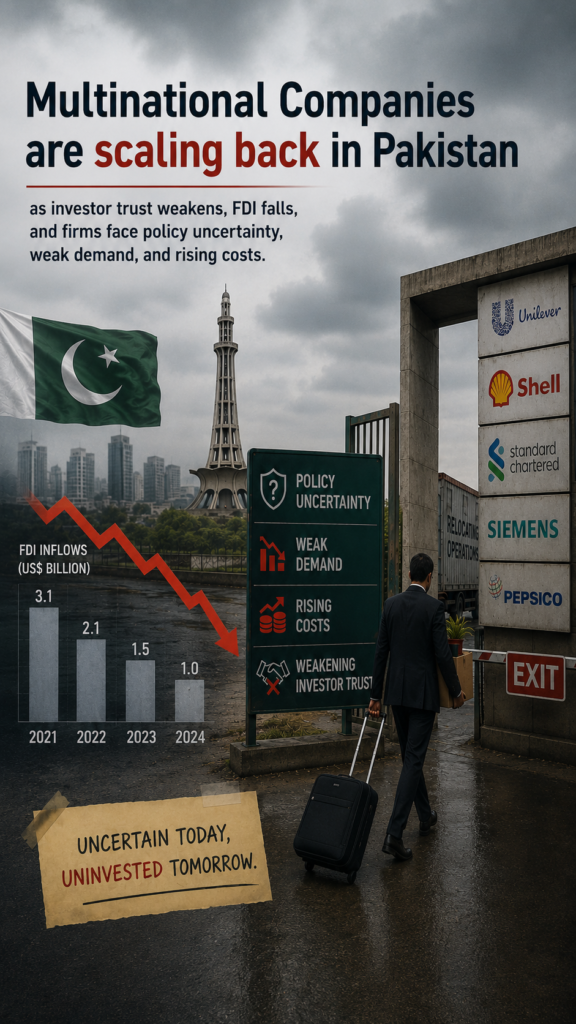

Top Multinational Companies Leaving Pakistan Since 2022

Why Multinational Companies cut back in Pakistan, and why trust keeps falling.

")

Introduction

Multinational Companies do not quit a market after one bad quarter. Usually, they leave after repeated policy shocks. Pakistan has now seen that pattern across many sectors. Tech, energy, telecom, pharma, and consumer goods appear on the list. However, that does not mean every firm vanished overnight. However, it does show a clear retreat in direct foreign commitment since 2022.

The macro picture is mixed. Inflation cooled, and official forecasts improved. However, investor trust still looks thin. SBP data show direct investment fell sharply in Jul-Apr FY26. It dropped to $1.409 billion, from $2.035 billion a year earlier. Total foreign investment almost vanished. It fell to just $31.7 million. Meanwhile, OICCI showed better headline confidence. Yet manufacturing barely improved. Firms still feared higher taxes, weak demand, and thinner margins. This gap explains why many MNCs remained cautious.

Who left and why

Not every case looked the same. Some MNCs sold equity stakes. Others closed apps, offices, or plants. Still, the signal looked similar. Pakistan became harder to justify for global boards. That is the story behind the biggest exits and wind-downs below.

Uber and Careem.

Uber started its retreat in October 2022. It shut its app in five cities and shifted riders to Careem. In April 2024, the Uber app also left Lahore. Uber framed the move as overlap reduction and a search for sustainable growth. Careem then suspended its Pakistan ride business in 2025. Its chief executive blamed a hard macro economy, stronger competition, and tighter capital allocation. This was a direct warning from the digital side of the economy.

Shell and TotalEnergies.

Shell announced the sale of its 77 percent stake in 2023. The company said it wanted to simplify its portfolio. Reuters also cited losses from rupee devaluation. It highlighted exchange-rate pressure, overdue receivables, and the broader slowdown. TotalEnergies then agreed to sell its 50 percent stake in Total PARCO in 2024. It said the move fit a strategy focused on core geographies with better growth and transition prospects. Two global energy names are cut back within a year. That looked less like chance and more like a pattern.

Telenor.

Telenor sold Telenor Pakistan to PTCL after a strategic review that began in 2022. The group said the sale fit its Asia strategy and favored scale. It also said local consolidation could strengthen Pakistan’s telecom market. By December 2025, Telenor completed the transaction. This was not a distressed collapse. However, it still meant a major foreign telecom no longer wanted Pakistan as a direct operating bet.

Sanofi and Pfizer.

Sanofi transferred its 52.87 percent stake in Sanofi Pakistan in 2023. The Company said it was not abandoning the market. Instead, it chose a different model to keep medicines available. Pfizer also moved away from direct local manufacturing. In 2024, Lucky Core signed agreements to buy Pfizer’s Karachi facility and several brands. Pfizer did not publish one simple Pakistan-only reason. However, the move came after Reuters reported severe margin stress across pharma from inflation, rupee weakness, import suppression, and delayed price relief. That makes the shift look more like de-risking than expansion.

Microsoft.

Microsoft closed its local operations in 2025 after 25 years. The company told TechCrunch it would serve customers through resellers and nearby offices. Pakistan’s IT ministry called it a partner-led, cloud-based shift rather than a full market retreat. That nuance matters. Yet the local office still closed, and direct headcount is still disappearing. Symbolically, this one hit hard. When a global software giant prefers a remote model, investors ask why an on-ground presence no longer makes sense here.

P&G and Lotte Chemical.

P&G decided in 2025 to discontinue its Pakistan business under a global restructuring plan. Reuters said it would wind down manufacturing and commercial activity, then rely on third-party distributors. Lotte Chemical also sold about 75 percent of its Pakistani subsidiary in 2025. Lotte linked that sale to a wider restructuring drive in South Korea’s loss-making petrochemical sector, hit by weak demand and oversupply. One move came from global restructuring. The other came from industry stress. Still, both reduced foreign industrial commitment to Pakistan.

What policy got wrong

Pakistan’s policymakers often chose emergency control over stable reform. To protect reserves, officials-imposed import bans and tight external-payment controls. Those steps did cut the current account gap. However, Reuters reported that they also hit raw materials and forced plant closures in sectors like cars and phones. The IMF later pushed Pakistan to remove such restrictions, restore a market-determined exchange rate, and unwind controls that had throttled growth. Short-term fixes bought time. They also damaged business trust.

Energy policy also kept punishing production. The IMF put power circular debt at Rs1.764 trillion in early 2026. It put gas circular debt at Rs3.442 trillion. The Fund also said lower structural energy costs would improve competitiveness and reduce fiscal risk. Reuters had already described the power debt crisis as a drag on supply, liquidity, and investment. Businesses do not need abstract theory here. They face high tariffs, delayed adjustments, and unstable cost assumptions every month. That is bad policy for any serious investment destination.

The Rising Cost of Policy Uncertainty

Taxes and regulations then made the problem worse. OICCI’s 2025 perception survey said foreign investors still worried about policy inconsistency and sudden shifts. OICCI’s 2025 business confidence survey said firms expected higher taxation, weaker demand, and reduced margins, even as overall confidence improved. A U.S. investment climate review also flagged red tape, weak rule of law, and ever-changing taxation policies. Investors can survive a tough market. They struggle in a market where rules move without warning.

In some sectors, the state also squeezed basic commercial viability. Reuters reported in 2023 that pharma firms struggled to stem losses from soaring inflation and a weaker rupee. Industry output had already dropped sharply. Some firms had fully shut down. Others had cut output. Companies blamed delayed price adjustments, import curbs, and rising input costs. When that happens, MNCs stop seeing regulation as protection. They start seeing it as unpriced risk.

Why this hurts the future

These exits matter because they shrink direct foreign presence in sectors that shape daily economic life. Careem helped normalize app-based transport and digital payments. Telenor brought connectivity to underserved regions. Microsoft linked Pakistan to global software ecosystems. When such firms reduce their local footprint, Pakistan loses more than one balance sheet. It loses signals, habits, talent pipelines, and confidence. Therefore, the reputational damage can outlast any single deal.

Pakistan’s economy is not in straight-line collapse. The IMF approved fresh funding in May 2026. The central bank also argued that recovery had broadened. However, the investment numbers still look harsh. Direct investment fell about 31 percent in Jul-Apr FY26. Total foreign investment fell from $1.460 billion to $31.7 million over the same period. So, the core problem is credibility. Stabilization improved. Trust did not fully return.

Local businesses feel this too. OICCI found that manufacturing confidence rose by only one point in Wave 28. The same survey said firms still feared taxation, weak demand, and squeezed margins. So, the problem is not only about foreign boardrooms. Domestic investors also struggle to plan long term when taxes, energy costs, and market rules stay uncertain. Therefore, the hit to the Pakistan economy runs deeper than a few famous exits.

Conclusion

Four failures sit behind this debacle. First, policy instability. Second, high energy costs and circular debt. Third, dollar shortages, import barriers, and weak payment confidence. Fourth, sector rules that crush margins, especially in pharma and formal consumer business. These were not minor irritants. They changed the basic risk math for MNC’s and local firms alike.

Pakistan can still attract Multinational Companies. However, it must stop treating every exit as an isolated case. Fresh MNCs will wait, and existing investors will stay light, unless the state offers stable taxes, predictable regulation, open access to inputs, and competitive energy. Local businesses need the same certainty. Multinational Companies do not demand perfection. They demand trust, and trust now looks too scarce in Pakistan.